Volatility in oil prices makes investing in the energy sector a risky proposition. The collapse in oil prices following the OPEC meeting in November 2014, at which Saudi Arabia announced its intent to flood the market to put American shale oil producers out-of-business, resulted in a rout in energy equities prices.

The Energy Select SPDR ETF (XLE) fell by 37 percent from November 26, 2014, to January 20, 2016. For many investors, the drop had become too large to sustain, and they closed their positions, locking-in a substantial loss.

XLE has recovered its loss, and as of July 27th, the price was nearly identical to its value on November 26th, 2014. But the recovery in oil prices, due to heightened geopolitical risks, also makes them vulnerable to another downward correction.

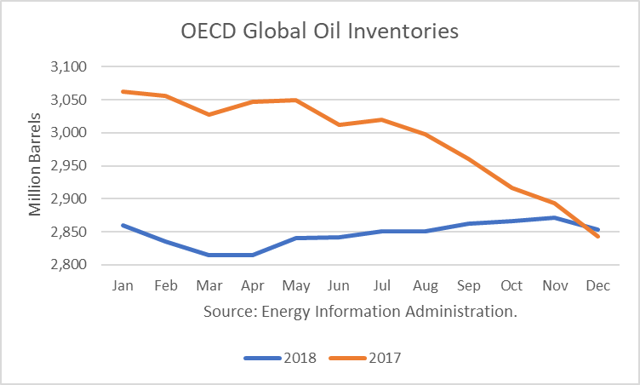

Citicorp, for example, issued a forecast proclaiming that “the bull argument is based on a faulty analysis,” and that oil prices “will fall back into a band between US$45 and US$65 in just over a year.”This raises the question of whether investing in the energy sector represents an attractive risk-reward opportunity. Continue reading "Hedging Energy Sector Oil Price Risk"