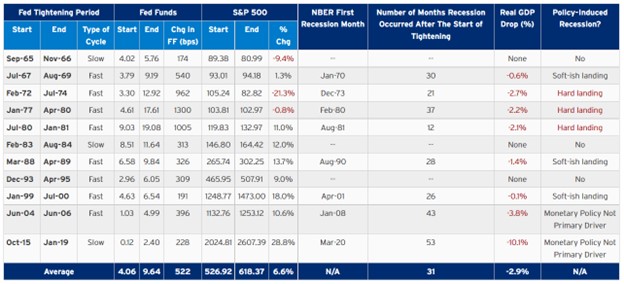

For those new to the game, the "Fed put" is a belief among investors that the Federal Reserve will come to the rescue anytime the stock market drops a certain amount. While much of the belief in the Fed Put is based on wishful thinking, it has proven to be the case enough times over the past 35 years or so that many investors have come to expect it.

Belief in the Fed put dates back to former Fed chair Alan Greenspan, who lowered interest rates and eased monetary policy numerous times during market turmoil, starting with the 1987 stock market crash. Since then, all his successors have followed the same basic policy, from Ben Bernanke to Janet Yellen to Jerome Powell, from the 2001 terrorist attacks to the 2008 global financial crisis to the 2020 coronavirus outbreak.

Of course, nearly all of those examples of the Fed put occurred during periods of benign inflation, when the Fed felt safe lowering interest rates to zero and injecting enormous amounts of money into the economy without fear of igniting price increases. Now, however, we live in a world of 8% inflation, and the Powell Fed has stated quite clearly that battling inflation is Priority No. 1, practically its only mission at the moment.

Indeed, when the S&P 500 fell 18% between reaching its all-time high of 4766 on December 27 through the recent low of 3901 on May 16 (the plunge in NASDAQ was even worse), the Fed sat on its hands, indicating the put is no longer suitable in this environment.

But since then (as of June 8) the S&P has rallied more than 6%. Is that a sign that some market watchers believe the Fed is once again going to exercise its put, or was it merely a dead cat bounce or buying the dip (or whatever you want to call it) on the road to even lower stock prices? Continue reading "Is the Fed Put Kaput?"