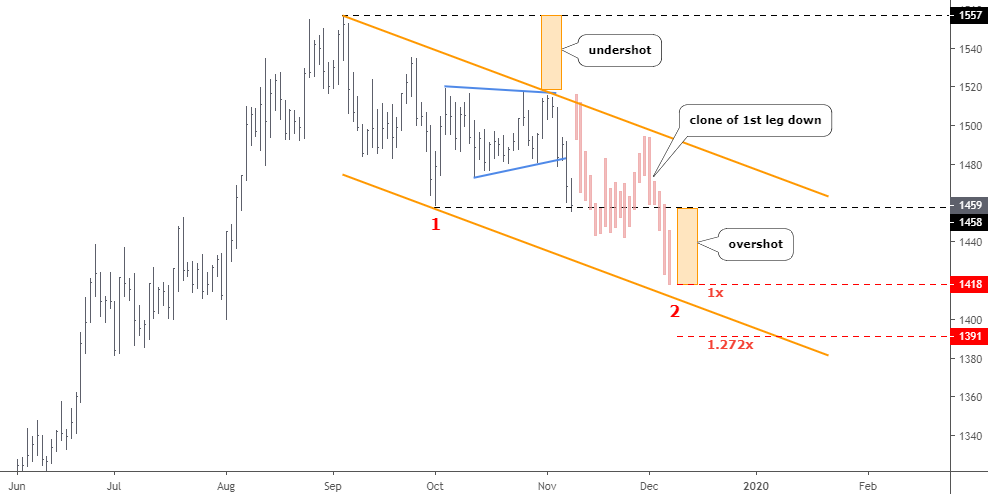

Gold bugs will remember 2012 as the last year of hope that gold was still in its bull cycle as it managed to hold key support around 1550 into year-end. It should not be lost on us that here into year-end 2019 gold’s new bull cycle has risen to, and logically halted at, the very same former support that is now important resistance to a new bull market.

We anticipated this resistance in the summer, and although the up-turning Semi cycle of 2013 was logical to gold’s demise 7 years ago, that is no longer the case as Semiconductor leadership takes a new leg up in 2019. Why? Well, let’s explore just a few of the differences between then and now.

Difference #1: The Yield Curve

The post-crisis era into 2012 was “inflation all the way baby!” as so well stated by my friend, the late Jonathan Auerbach back in Q4 2008. It was monetary fire hoses all day every day and policy makers didn’t care who knew it. There was a major systemic meltdown of the previous inflation in play and of course, our heroes at the Fed fought that realized risk with more of what created it in the first place, balls-out inflationary policy.

The crowning achievement – and gold killer – of post-crisis policy was 2011’s Operation Twist and its stated mission of controlling the yield curve, as Twist’s agenda to buy long-term Treasury bonds and sell short-term Treasury bonds was the very essence of a flattener. That cannot be disputed. Bernanke kicked off the great flattening and gold was done for years to come. Continue reading "Today vs. 2012; Different This Time For Gold"