Thank you for your interest in this exclusive analysis and INO.com's Daily Analysis & Commentary. Please see the report below and don't hesitate to contact us at

su*****@in*.com

if you have any questions. You can also view this Traders Blog for daily analysis, trading polls, and complimentary tools.

Published 10AM, April 8th, 2014

I have to be honest with you: When I drilled down into the nuts and bolts of CVS Caremark (CVS), I couldn't believe my eyes: This pharmacy and retail drugstore giant boasts a fantastic blend of outstanding fundamentals, great valuation, and an exciting technical picture.

Bigger Is Sometimes Better

Let's get right to it: Bigger is sometimes better. And when it comes to a leading company in the retail drugstore, pharmacy benefit management (PBM), and retail health clinic space, you can stop your search at CVS.

First off, the company is the largest pharmacy health care provider in the U.S. with a whopping 7,600 CVS/pharmacy retail stores, 1.6 billion prescriptions filled, and 63 million PBM plan members. In addition, its retail health clinic system boasts about 800 MinuteClinic locations. Talk about a pharmacy retail powerhouse!

But that's not all. CVS is also a market leader in mail order, Medicare Part D Prescription drug plans, and specialty pharmacy practices. The company is one of the most innovative pharmacy retailers out there, actively developing new ways to improve healthcare costs and efficacy, including its cutting-edge Pharmacy Advisor program.

All told, you'd be hard pressed to find a more dominant player in the drugstore and pharmacy space. But CVS's work doesn't stop there: The company also boasts one of the strongest fundamental outlooks I've seen in a drugstore retailer in a long time.

CVS Packs Outstanding Fundamentals

Last year, CVS drove top line revenues to a record $127 billion, up 3% from $123 billion in 2012. And contributing to that growth was solid revenue generation from both of the company's operating segments: In 2013, CVS's Retail Pharmacy segment punched up top line revenues 3.1% to $66 billion while the company's Pharmacy Services segment increased sales 3.8% to $76 billion.

As first glance you may look at this revenue numbers and go away unimpressed. After all, growth in the 3% to 5% area isn't exactly mind-blowing. But in the realm of massive, established companies like CVS, top-line growth in this area is just what you'd expect.

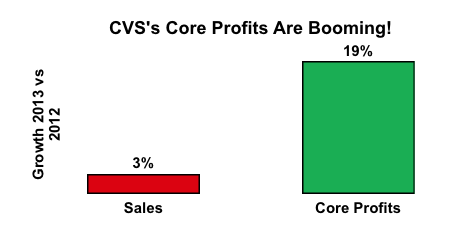

But that's not the whole financial story at CVS. Just like any large, established company, CVS's real kudos comes from what profits it can generate from modest revenue increases. And here the news is great. Take a look...

As you can see from this chart, while CVS grew its top line 3% in 2013 compared to 2012, its core profits -- or profits from its on-going operations -- jumped from $3.9 billion to $4.6 billion. That amounts to a whopping 19% increase in profits from the company's core operations -- over 6 times the growth rate of sales! No doubt about it, that points to a well-managed and fine-tuned large company.

But that's not all. All told the company produced earnings-per-share (EPS) of $4.00 a share during 2013. Estimates are calling for CVS to $4.47 in EPS in 2014 and another $5.01 EPS in 2015. Compared to 2013's $4.00 a share, those increases amount to a 12% increase in 2014 and 2015. No two ways about it, that's a solid earnings outlook!

CVS Kicks The Habit

Earlier this year, CVS announced that it would stop selling tobacco products in its 7,600 locations by October, 2014. And no matter how you slice it, the move is right on target.

First off, the announcement had no negative effect on the stock price. In fact, take a look a chart of CVS and you can see how, since the stop-smoking announcement, the stock has been pretty much on a tear. So, no real worries from investors about the news.

Fundamentally, a tobacco-free CVS will generate about $2 billion less in annual sales. Compared to annual sales in 2013 of $127 billion, that's not much to fret about. Factor in the good will and general healthcare brand appreciation the move will generate and the news is even better. According to Helena Foulkes, president of the company's pharmacy business...

"We are seeing this tobacco decision as an opportunity to connect even more with consumers as an expert in health and beauty and to build our loyalty with them."

The move should also help bring in business, especially as CVS continues to court accountable care organizations (ACOs) -- organizations that focus on healthcare outcomes and cost containments -- that have trumpeted the negative role tobacco plays on exacerbating chronic illness.

Growth In Health Coverage A Huge Plus For CVS

By 2016, estimates are calling for the Affordable Care Act to extend health insurance to a whopping 25 million people. In fact, so far the law has generated the greatest expansion in healthcare coverage since 1965. Certainly, the law faces challenges: In fact, rate increases next year could put a bucket of cold water on the process. But no matter how you look at the law, the massive increase in health care coverage means big bucks for CVS.

CVS Is A Dividend Machine

Currently, CVS pays $1.10 a year in dividends to shareholders. Compared to a recent price of $74, that amounts to 1.5% dividend yield. While that's not the best on the block, it compares very favorably with the 1.96% dividend yield of the S&P 500.

But that's not the whole dividend story at CVS. The company has managed to increase dividends each and every year for the past 11 years. That's impressive and no small feat, especially when you consider the ups and downs the economy has been through over the same period. Plus, dividends are still one of the most attractive aspects for the average stock investor. And that's a big plus for share value going forward.

CVS Is Priced To Move Higher

Take a spin around any of the research I do and you can't help but notice that in some ways I'm a creature of habit. And that's especially true when it comes to valuing a stock. I always look at a company's price to earnings ratio (P/E) ratio. While the ratio informative in and of itself, it's also a great way to compare share prices of companies in an industry or across industries. Here, again, CVS is a winner. Take a look...

CVS currently trades at a P/E ratio of 19.9. Compared to the S&P 500's P/E ratio of 17.7, CVS is a bit pricey compared to the broader market. But factor in the outstanding fundamentals we've talked about and I think it's a good buy.

Now, take that same P/E for CVS and compare it to the sector's P/E ratio of 33.4 and the story changes big-time. In fact, with CVS projected to earn $4.47 in 2014, its sector-generated share price should be around $149 a share over the next year. While I doubt CVS's share price will climb that high that quickly, the momentum is certainly to the upside and not the downside.

CVS's Technical Outlook Is Outstanding

As you can see, the fundamental outlook for CVS is huge. But that's just part of the why I like this stock so much: The other part is simply an outstanding technical picture...

As you can see from this weekly chart of CVS's stock price, the technical news for CVS couldn't be better. In fact from a long term low of $32 -- marked way back in August 2011 -- the stock's trajectory has been pretty much straight up.

Now, there have certainly been pullbacks along the way: The chart clearly shows that the share price has struggled at times. And that's a good thing -- a stock that goes straight up all the time has caution written all over it.

How far will CVS's share price go from a technical perspective? No one knows for sure. But unless a dominant fundamental factor comes into play, a stock that has consistently reached new highs -- with natural pullbacks along the way -- should be poised to continue to move higher.

The Story on CVS Couldn't Be Better

CVS Caremark is a dominant company in the retail drugstore, pharmacy benefit management (PBM), and retail health clinic space. Its strong fundamentals are backed by solid top-line revenue growth, outstanding profit generation, and an attractive earnings outlook. The company consistently produces dividends for shareholders. Add in an outstanding technical outlook and it's clear that CVS is a company worth taking a strong look at.

I hope you enjoyed this report,

Wayne Burritt

Market Research Contributor

INO.com, Inc.

---

Wayne has over 29 years of experience in financial writing, investment analysis, and business

development. Before starting Burritt Research, Inc. Wayne was a senior equity research analyst

and editor for Weiss Research, a nationally acclaimed independent research and advisory firm.

He directed all fundamental and editorial aspects of a variety of domestic and international

option and stock services. Prior to his tenure at Weiss, Wayne was an equity analyst, marketing

and trading specialist for Pan-American Financial Advisers, a boutique investment management

firm. He provided security analysis, marketing support, and trading services for a large portfolio

team engaging institutional and high net worth clients. Wayne also produced and starred in the

critically acclaimed stock market radio show Inside the Market while at Pan-American Financial.

Wayne has also held positions as Managing Director, Senior Credit Analyst, and Controller. He

holds an MBA from Golden Gate University and a BA in English and Philosophy from Indiana

University.

---

MarketClub is owned and operated by INO.com INC (hereafter referred to as “INO”). INO is not a registered broker dealer or a registered investment advisor. No information accessed through the INO.com website or any newsletter constitutes a recommendation to buy, sell or hold any security in any jurisdiction. Please consult a broker before purchasing or selling any securities viewed or mentioned herein. INO has made every reasonable effort to ensure that the information and assumptions on which these statements and projections are based are current, reasonable, and complete. However, a variety of factors could cause actual results to differ materially from the projections, anticipated results or other expectations expressed in this release. INO makes these statements and projections in good faith, neither INO nor its management can guarantee the accuracy of some of the content in this release containing for-ward-looking information within the meaning of Section 27 A of the Securities Act of 5/27/33 and Section 21 E of the Securities Exchange Act of 6/6/34 including statements regarding expected continual growth of the profiled company and the value of its securities. In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1 995 it is hereby noted that statements contained herein that look forward in time which include everything other than historical information, involve risk and uncertainties that may affect a company’s actual results of operation. A company’s actual performance could greatly differ from those described in any forward looking statements or announcements mentioned in this release. Any investment in a company profiled by us should be made only after consultation with a qualified investment advisor and review of the publicly available financial statements and other information about the company profiled in order to verify that the investment is appropriate and suitable. Information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete.