Options trading can provide a meaningful addition to one's portfolio when used in a disciplined manner. When used as a component of an overall portfolio approach, generating consistent monthly income while defining risk, leveraging a minimal amount of capital, and maximizing return on capital can be achieved. Options can enable smooth and consistent portfolio appreciation without guessing which way the market will move. An options-based portfolio can provide durability and resiliency to drive portfolio results with substantially less risk via a holistic beta-controlled manner. When engaging in options trading, specific rules must be followed, and one of the most important rules is to structure every option trade in a risk-defined (put spreads, call spreads, iron condors, etc.) manner.

PayPal (PYPL) was a recent example where the stock witnessed a massive meltdown from an ill-advised acquisition target (Pinterest) coupled with quarterly earnings that were deemed dismal. These two events culminated into a 35% slide from a 52-week high of $310 down to ~$200 post-earnings. Hence the importance of risk-defining all options trades to limit any downward stock movement beyond your protection strike. Risk-defined options trading prevents any losses beyond a specific strike price, avoids the assignment of shares, does not require a significant amount of capital, and does not potentially result in unrealized losses while soaking up capital with any share assignments.

Risk-Defined Options Trading

Risk-defined option trades are straightforward. Below is a theoretical example deploying a put spread on a stock that currently trades at $100 per share.

-

1. Sell a put at a $95 strike and collect $1 per share in premium – You take on the obligation to buy shares for $95 by the expiration date and receive $100 in option premium income.

2. Buy a put at a strike of $90 by using some of the premium received (e.g., $0.40 per share) – You have the right to sell shares at $90 a share by the expiration date.

In the above put spread scenario, premium income was $60 per contract ($1.00 - $0.40) and the maximum risk was $440 ($95 - $90 = $500 - $60 of net premium income). If the shares remain above $95 by the expiration date, then the option expires worthless, and the seller of the put spread locks in a realized gain of $60 or a return on investment of 13.6% ($60/$440). This is the essence of risk-defined options trading, where a minimal amount of capital is leveraged and return on investment is maximized.

No matter where the stock moves, losses are capped at $440 per contract even if the underlying stock falls to zero. This is the case due to the protection put leg that was purchased at the $90 strike. Therefore, in the worst-case scenario, if the stock were to fall to zero, you would be assigned shares at $95 and then sell the shares for $90 for a max loss of $5 per share less the $0.60 in premium, thus max loss of $440 per contract.

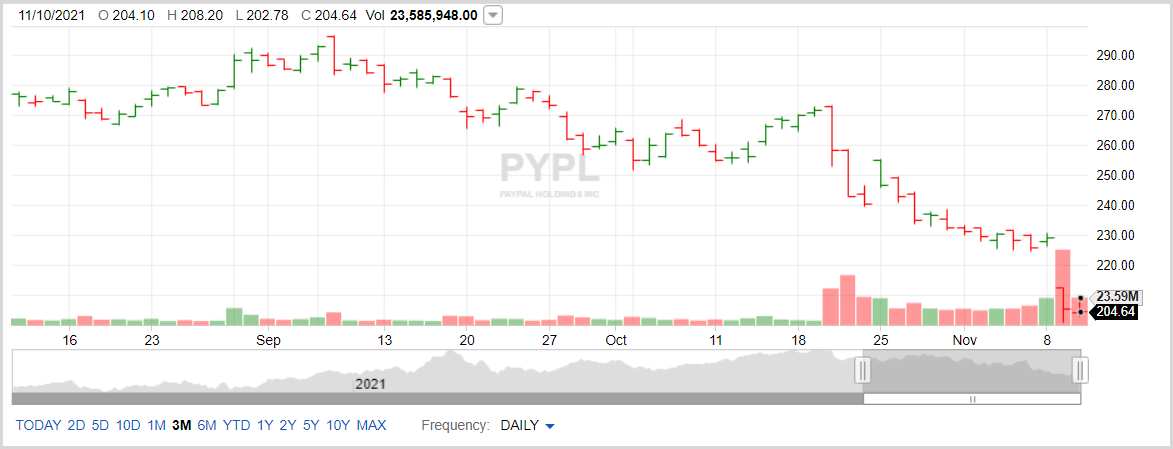

PayPal Case Study

PayPal (PYPL) experienced a dramatic fall from $296 on September 8th to ~$200 on November 10th after a two-step debacle of a mishandled acquisition target and a big earnings miss. This 32% downslide happened over the course of 8 weeks. A put spread of $245/$240 was sold on PayPal, and a near max loss was suffered. However, the $40 additional dollars per share in unrealized losses were avoided with the $240 protection strike. In a cash-covered put situation, shares would've been assigned at $245, and a subsequent ~20% loss would've been incurred. Cash-covered puts can not only be dangerous in situations like this but can also tie up substantial amounts of capital with unrealized losses. Therefore, a risk-defined put spread was essential in order to protect downside risk and avoid any capital-intensive assignment of shares.

Figure 1 – The importance of risk-defined options trades such as put spreads, call spreads, and iron condors which is the foundation of options trading - Trade Notification Service and Options Screening Tool

10 Rules for an Agile Options Strategy

A disciplined approach to an agile options-based portfolio is essential to navigate pockets of volatility and circumvent market declines. A slew of protective measures should be deployed if options are used to drive portfolio results. When selling options and managing an options-based portfolio, the following guidelines are essential (Figure 3):

-

1. Trade across a wide array of uncorrelated tickers

2. Maximize sector diversity

3. Spread option contracts over various expiration dates

4. Sell options in high implied volatility environments

5. Manage winning trades

6. Use defined-risk trades

7. Maintains a ~50% cash level

8. Maximize the number of trades, so the probabilities play out to the expected outcomes

9. Place probability of success in your favor (delta)

10. Appropriate position sizing/trade allocation

Conclusion

An options-based portfolio can provide durability and resiliency to drive portfolio results with substantially less risk via a holistic beta-controlled manner. When engaging in options trading, specific rules must be followed, and one of the most important rules is to structure every option trade in a risk-defined (put spreads, call spreads, iron condors, etc.) manner. Therefore, a beta-controlled, options-based strategy is key, and the market meltdown in September reinforces why appropriate risk management is essential. An options-based approach provides a margin of safety while circumventing drastic market moves while containing portfolio volatility.

PayPal (PYPL) was a recent example where the stock witnessed a massive meltdown from an ill-advised acquisition target coupled with poor quarterly earnings. These two events culminated into a 35% slide from a 52-week high of $310 down to ~$200 post-earnings. Hence the importance of risk-defining all options trades to limit any downward stock movement beyond your protection strike. Risk-defined options trading prevents any losses beyond a specific strike price, avoids the assignment of shares, does not require a significant amount of capital, and does not potentially result in unrealized losses while tying up large sums of capital with share assignments.

Noah Kiedrowski

INO.com Contributor

Disclosure: Stock Options Dad LLC is a Registered Investment Advising (RIA) firm specializing in options-based services and education. There are no business relationships with any companies mentioned in this article. This article reflects the opinions of the RIA. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. The author encourages all investors to conduct their own research and due diligence prior to investing or taking any actions in options trading. Please feel free to comment and provide feedback; the author values all responses. The author is the founder and Managing Member of Stock Options Dad LLC – A Registered Investment Advising (RIA) firm www.stockoptionsdad.com defining risk, leveraging a minimal amount of capital and maximizing return on investment. For more engaging, short-duration options-based content, visit Stock Options Dad LLC’s YouTube channel. Please direct all inquires to

in**@st*************.com

. The author holds shares of AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY, and USO.

You didn't mention the margin requirements for put spreads (or other option trades).

Hi Noah, thank you for your article. Very appropriate as I just sold a vertical spread on PayPal. Thanks Dave