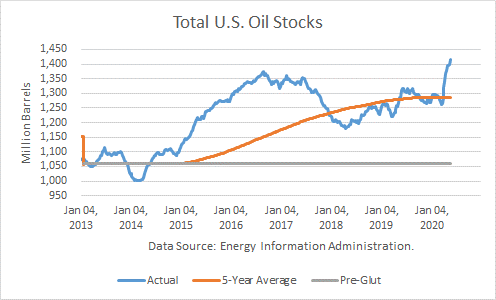

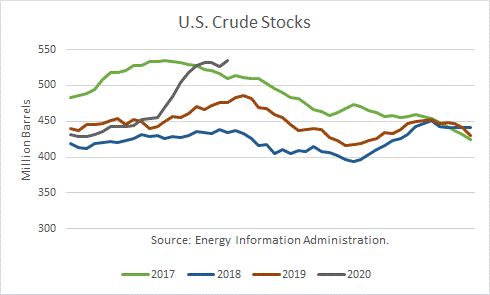

According to the Energy Information Administration, U.S. crude inventories (excluding SPR) built by 14.9 million barrels last week to 1.415 billion, whereas SPR stock built by 2.1 million. They stand 129 mmb above the rising, rolling 5-year average and about 129 mmb higher than a year ago. Comparing total inventories to the pre-glut average (end-2014), stocks are 356 mmb above that average.

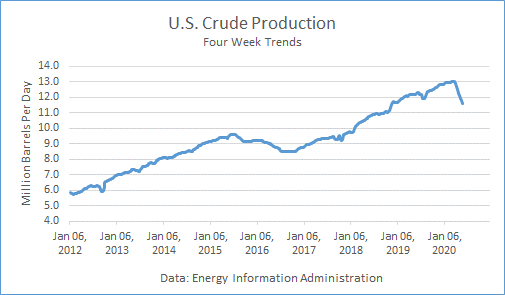

Crude Production

Production averaged 11.400 mmbd last week, down 100,000 b/d from the prior week, and 11.600 mmbd over the past 4 weeks, off 4.9 % v. a year ago. In the year-to-date, crude production averaged 12.580 mmbd, up 4.2 % v. last year, about 500,000 barrels per day higher than a year ago.

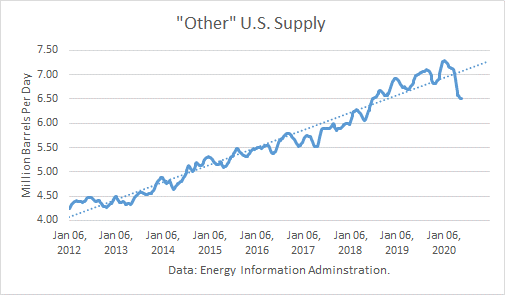

Other Supply

The EIA reported that it rose by 67,000 b/d v. last week at 6.529 mmbd. The 4-week trend in “Other Supply” averaged 6.499 mmbd, off 6.2 % over the same weeks last year. In YTD, they are 1.5 % higher than in 2019.

Crude oil production plus other supplies averaged 18.099 mmbd over the past 4 weeks, well below the all-time-high record.

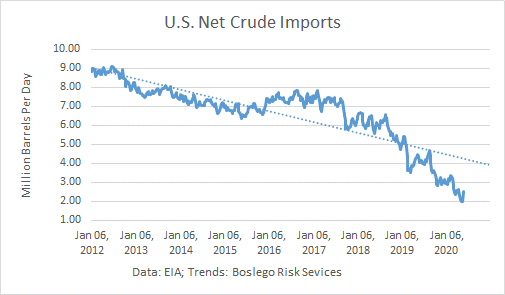

Crude Imports

Total crude imports rose by 2.003 mmb/d last week to average 7.200 mmbd last week. This figure was above the 4-week trend of 5.875 mmbd, which in turn was off 16.4 % from a year ago.

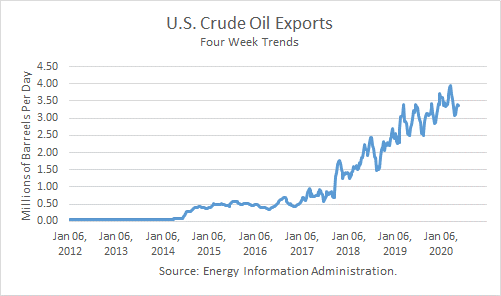

Net crude imports rose by 2.066 mmb/d because exports fell by 63,000 b/d to average 3.176 mmbd. Over the past 4 weeks, crude exports averaged 3.372 mmbd, 13.3 % higher than a year.

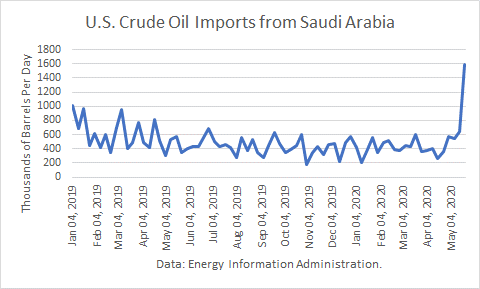

U.S. crude imports from Saudi Arabia rose by 947,000 last week to average 1.590 mmb/d. This reflected the surge in Saudi exports to the U.S., which began in late March after the price began between the Saudis and Russians. They had reportedly sent an armada of tankers carrying up to 50 million barrels to flood the U.S. market. Over the past 4 weeks, Saudi imports have averaged 840,000 b/d, up 91 % from a year ago.

Crude imports from Canada rose by 328,000 b/d last week, averaging 3.274 mmbd. Imports over the past 4 weeks averaged 3.072 mmbd, off 11.2 % v. a year ago.

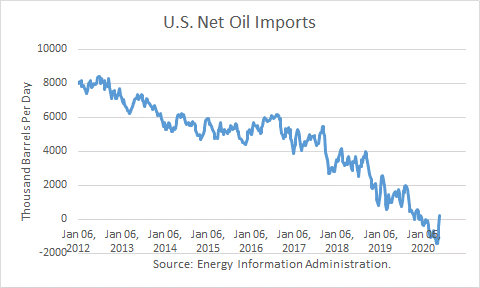

Net oil imports averaged 236,000 b/d over the past 4 weeks. That compares to net oil imports of 1.345 mmbd over the same weeks last year. This is the first 4-week period this year in which imports exceeded exports.

Crude Inputs to Refineries

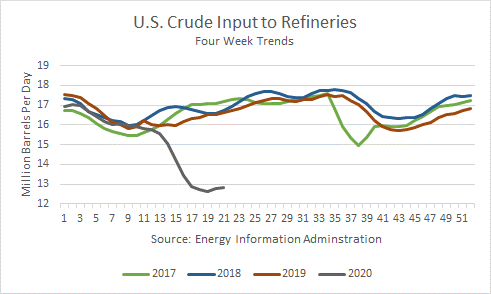

Inputs rose by 87,000 b/d last week averaging 12.991 mmbd. Over the past 4 weeks, crude averaged 12.813 mmbd, off 22.8 % v. a year ago. In the year-to-date, inputs averaged 14.765 mmbd, off 9.6 % v. a year ago.

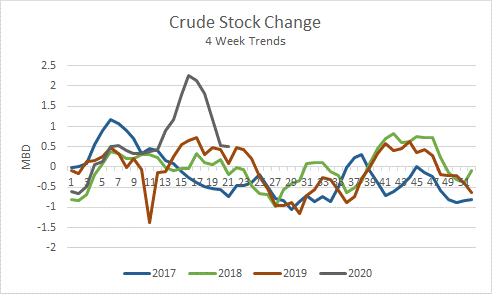

Crude Stocks

Over the past 4 weeks, crude oil supply exceeded demand by 515,000 b/d.

Commercial crude stocks 534.4 mmb are now 57.9 million barrels higher than a year ago.

Petroleum Products

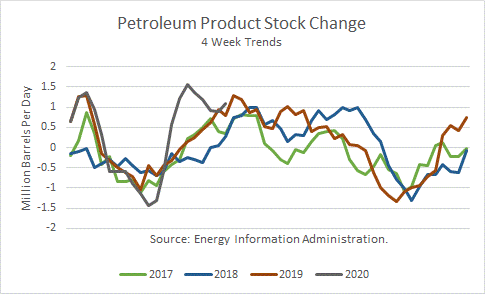

Given the recent net product stock builds, product supply has exceeded demand by 1.089 mmb/d.

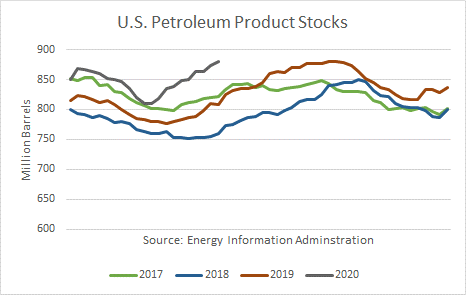

Total U.S. petroleum product stocks at 880 mmb are 71 million barrels higher than a year ago.

Product exports rose by 667,000 b/d last week, averaging 4.347 mmbd. The 4-week trend of 4.072 mmbd is off 21.8 % from a year ago. In the year-to-date, exports averaged 5.234 mmbd, up 3.1 % from a year ago.

Demand

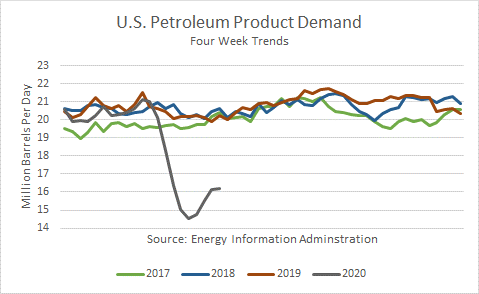

Total petroleum demand averaged 16.178 over the past 4 weeks, off 20.1 % v. last year. In the YTD, product demand averaged 18.317 mmbd, off 10.8 % v. the same period in 2019.

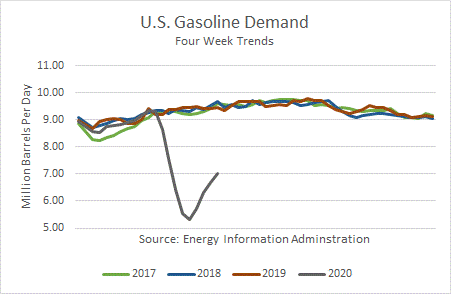

Gasoline demand at the primary stock level fell by 431,000 b/d last week and averaged 7.026 mmbd over the past 4 weeks, off 25.7 % v. the same weeks last year. In the YTD, it reported that gas demand is off 15.7 % v. a year ago.

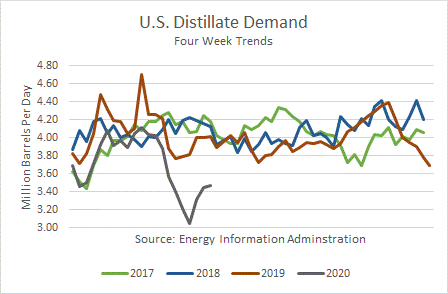

Distillate fuel demand, which includes diesel fuel and heating oil, fell by 402,000 b/d last week, and averaged 3.470 mmbd over the past 4 weeks, off 13.6 % v. the same weeks last year. In the YTD, demand is off 9.6 % v. a year ago.

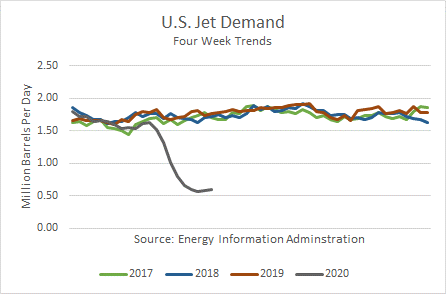

Jet fuel demand is off 66.6 % over the past 4 weeks v. last year. In the year-to-date, demand was off 30.3 % v. 2019.

Product Stocks

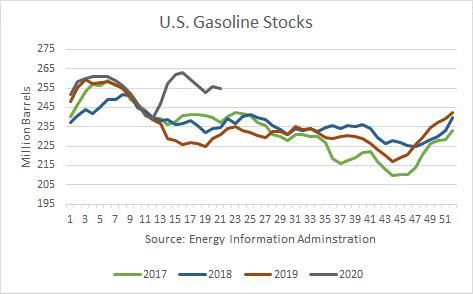

Gasoline stocks are now 24.1 mmb higher than a year ago, ending at 255.0 mmb.

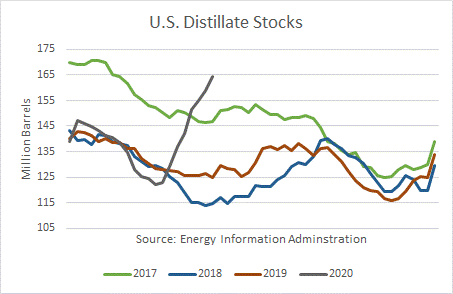

Distillate stocks are 39.5 mmb higher than a year ago, ending at 164.3 mmb.

Conclusions

The bottoms in petroleum product demand and crude oil demand at refineries are clearly seen in the graphs. However, both crude and product stocks continue to rise as supplies still exceed demand.

Furthermore, the Saudi import surge has just been recorded in the customs data. We can expect to see the surge continue for another 3 weeks, ballooning crude stocks.

Oil prices have rebounded off the lows, but the oil market is not out of the woods yet. And it remains to be seen how robust the oil demand rebound will be with high unemployment and behavioral shifts due to the pandemic affecting oil demand.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

i would like to hear when it's a good time to buy oil stocks.

better go higher asap